Liberty TripAdvisor Holdings ($LTRPA)

Microcap holdco with multi-bagger potential and a catalyst

Disclosure: I have a beneficial long position in the shares of Liberty Tripadvisor Holdings, Inc. (NASDAQ: LTRPA). I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All content on this newsletter, and all other communication and correspondence from me, is for informational and educational purposes only and should not in any circumstances be considered to be advice of an investment, legal or any other nature. Please carry out your own research and due diligence.

If you only have a few seconds, the following is a summary of the thesis:

TripAdvisor (TRIP) is the world's largest travel platform, with almost half a billion unique users, one billion reviews, and millions of listings of accommodations, travel activities and experiences, and restaurants

It is in the early innings of a business transformation towards a subscription model, which could see it become the low-cost producer in the industry

Recent issues with the execution of its business transformation have caused the market to penalize TRIP shares

Nevertheless, the value of the business as it exists today offers significant downside protection should the transition to a subscription model fail

Its core metasearch business is highly cash-generative, offering an 11% FCF yield on my 2022 estimates. It also owns Viator, the world's largest online travel agency in tours & attractions, and TheFork, the largest online restaurant reservations platform in Europe, Australia, and Latin America

Management has announced it is exploring options to sub-IPO Viator, which provides a potential catalyst for the stock

The company recently refreshed its management team to better execute on its vision and is also backed by experienced and incentivized board members in Greg Maffei and Greg O'Hara

Based on a sum-of-the-parts valuation, I believe that TRIP could be worth 2.4x its current market cap, and Liberty TripAdvisor Holdings (TripCo), which owns 21% of TRIP, could be worth 10.3x its market cap

Introduction

Liberty TripAdvisor Holdings (TripCo) is a holding company that does not have any operations outside of its controlling interest in its publicly listed subsidiary, TripAdvisor (TRIP). TripCo owns approximately 21% of TRIP common stock and has a c.57% voting interest in the company.

TRIP has a market cap of $3.3 billion and an enterprise value of $3.2 billion. Based on its ownership of TRIP shares, TripCo has a net asset value (NAV) of $207 million and a market cap of $175 million. However, as I explain in the valuation section, TripCo's market cap is artificially inflated — it is actually closer to $91 million.

While this write-up aims to discuss the investment thesis behind TripCo's A Shares (LTRPA), I will spend much of the paper discussing and determining a reasonable fair value for TRIP, before returning to the valuation of TripCo based on its 21% stake in TRIP.

Business Overview

TRIP is an online travel company whose website, TripAdvisor.com, allows users to plan their trips and read reviews on various hotels, restaurants, and attractions. It is the world's largest travel platform by users, with almost half a billion unique users, one billion reviews, and millions of listings of accommodations, travel activities and experiences, and restaurants.

TRIP also operates Viator, the world's largest online travel agency (OTA) in tours and attractions, and TheFork, the largest online reservations platform in Europe, Australia, and Latin America. The company generates 78% of its revenues from TripAdvisor Core, 18% from Viator, and 8% from TheFork as of 2019 (I use 2019 because of the pandemic).

In terms of their respective business models, TripAdvisor Core is primarily a distribution channel for OTAs and hotels to list their accommodations. Most of its revenue is generated from click-based advertising for booking links to travel partner websites, priced on a cost-per-click (CPC) basis. Viator acts as the merchant of record and generates commissions for each booking transaction.TheFork primarily generates its commission from restaurants on a per-booking or per-seated diner basis for bookings made on the TheFork. TRIP has also been testing its Tripadvisor Plus subscription, an annual subscription-based membership that offers discounts and perks for 500,000+ hotels and experiences for $99/year.

In the following sections, I will briefly review TRIP's failed attempt to transform its business in 2014 before discussing its current efforts to transition to a subscription model. This will provide some helpful perspective in assessing the subscription model's ultimate chances of success.

Money (That's What I Want): Instant Booking

From 2009 to 2013, TRIP experienced a remarkable amount of growth, going from serving 36 million to 260 million monthly unique visitors and $352 million to $945 million in revenue. However, operating margins also started to deteriorate gradually during this time, falling from 48% to 31%. This occurred for several reasons, including increased competition from the likes of Google, Yahoo Travel, and Yelp, lower monetization from users on mobile devices, and costs of developing its mobile app and metasearch functionality.

Key among these issues was TRIP's problem with monetizing its customer base. Like many internet companies, TRIP essentially has two functions critical for their business: customer acquisition and conversion. That is, TRIP is successful to the degree that it can convince customers to visit its website at the lowest cost possible and convert as many of these visitors from lookers to bookers on its partners' (OTAs and hotels) websites to generate advertising fees.

Its problem was that users would browse the Tripadvisor website to read reviews and plan their trips but would then leave without clicking on their partners' booking links. Given that it can often times be difficult to track the user through to their booking (particularly across devices), TRIP was not getting its fair share of attribution for the bookings that it facilitated.

To address this issue and capture a larger share of the bookings pie, in 2014, TRIP introduced Instant Booking, which allowed users to book directly on Tripadvisor. This way, TRIP would get direct attribution for customers who use its website and also benefit from the higher-margin commission fee.

Unfortunately, the initiative failed since TRIP needed to convince more users to book directly on its website (i.e., conversion was not high enough). TRIP had gone from being a distributor of hotel bookings to a retailer of hotel bookings and was now responsible for closing the sale. This required very different skills. Successful OTAs like Booking Holding focus relentlessly on making hundreds of improvements to their websites, from features that reduce friction to those that entice the consumer to book. These small improvements add up over time to increase customer conversion to the 20%-25% range. At only 6% conversion, TRIP could not compete profitably.

At the same time, TRIP's prioritization of its Instant Booking links drew attention away from the links to book on the websites of the other OTAs and hotels, which motivated them to pull advertising spend away from TRIP's traditional metasearch platform. These issues combined to reduce revenue per hotel shopper from $0.58 in 1Q14 to $0.4 by 3Q17 and operating margins from 31% in 2013 to 8% by 2017. In response, management significantly curtailed Instant Booking in 2017.

Tripadvisor Plus: Instant Booking 2.0?

Skip forward to February 2021, and TRIP announced it would be rolling out TripAdvisor Plus, a subscription travel product that offers subscribers 10-30% upfront discounts and perks on bookings of hotels and experiences for $99/year. The initiative was pitched as a "no-brainer" by management, given that it provided customers with savings of $350, which more than covered the subscription fee on their first bookings.

TRIP estimated that it hosted 160 million hotel metasearch clicks for its target Plus audience of customers who book stays costing $750 or more per year. Converting just a small share of this customer base to $99 per year subscribers would provide upwards of $1bn in high-margin subscription revenue. The idea seemed very attractive, and investors piled into TRIP's stock accordingly, driving the price from about $30 in January 2021 to a peak of $60 in March 2021.

However, in September 2021, TRIP was forced to make changes to the model to appease the large hotel chains, which claimed that TRIP's open advertising of the discounts on its website violated their rate parity agreements with the OTAs. These agreements legally require hotels to offer the same rate for a room regardless of the distribution channel. Unfortunately, buy-in from the hotel chains was essential, given that they account for approximately 70% of all hotel accommodations in the US (in Europe, it's only 37%).

Rather than provide upfront discounts, the newly-revised TripAdvisor Plus model now centers on giving subscribers "vacation funds," which can be spent once customers have booked into their hotel (essentially a cashback model). The intuitive and psychological appeal to the customer is not as clear under this model, as it forces customers to delay gratification. As a result, it has yet to generate significant traction.

This setback was not received lightly by investors, who have sold off TRIP shares to their current levels of about $23. At current levels, TRIP shares seem to price in a zero percent chance of success for TripAdvisor Plus. The difficulties of transitioning to the subscription model have also evoked comparisons between TripAdvisor Plus and the failed Instant Booking initiative.

However, I remain optimistic about TripAdvisor Plus. Unlike Instant Booking, the offering has several benefits, both for TRIP and the customer. First of all, by developing a loyal customer base, which automatically goes to book on TripAdvisor to access discounts, the subscription model addresses the issues of conversion and customer acquisition that existed under the Instant Booking model.

Second, unlike for Instant Booking, there is a real value proposition to the customer under the subscription model. This is because TRIP takes the costs it saves on customer acquisition (most of which would go to Google) and shares them with the customer. These savings can be quite significant given that (1) customer acquisition costs for OTAs can range between 30%-60% of revenues and (2) travel is such a big-ticket purchase.

It may help to quickly run through the two models' unit economics to illustrate how TRIP's subscription model would work. Consider a customer that books a hotel for 5 days at $150 per day, for a total $750. In the traditional OTA model, the hotel may receive $500 and pay Booking Holdings (the OTA) a $150 commission. Out of that $150, Booking will pay $60 in advertising costs (primarily to Google). This will leave them with enough to cover $30 in other operating costs (personnel, G&A, IT, etc.) and earn $60 in EBITDA (or a 40% EBITDA margin).

Under the subscription model, the hotel would still receive the $500 and pay TRIP a $150 commission. However, TRIP would pass that $150 in savings to the customer in exchange for a $100 per year fee. Assuming the customer churns every 3 years, TRIP would only have to pay $20 in advertising costs ($60/3), which, after $30 in other operating costs, leaves them with a $40 in EBITDA (or a 40% EBITDA margin).

The benefits of transitioning to this model for TRIP are very clear. Under its current metasearch model, it probably earns $3 max in advertising revenue per customer. By contrast, every TripAdvisor Plus customer might be worth $40 in EBITDA. Interestingly, however, it also puts Booking Holdings in the innovator's dilemma, whereby replicating TRIP's subscription model would convert a customer worth $60 in EBITDA to one worth $40 in EBITDA.

Of course, the critical issue for TRIP is finding a method to successfully distribute the cost savings in a way that is attractive to the customer but does not violate rate parity. If it successfully does so, it could become the low-cost producer in the OTA industry.

One option that could make sense for TRIP would be to include TripAdvisor Plus as part of a bundle. This way, the significant customer savings that TRIP contributes could indirectly help increase the other subscriptions' affordability. It could particularly benefit from bundling its subscription with more habitual and frequently used subscriptions, such as Spotify, Netflix, or Amazon Prime, as this could also help reduce churn. In fact, TRIP has already been partnering with several other subscription services, including Rent the Runway, USA Today, Dollar Flight Club, Hertz, and The Weather Channel.

While there are always risks involved in any business model transformation, I remain optimistic about the potential for TripAdvisor Plus given its evident advantages. That being said, the investment does not rely on its success, given that the value of the business as it exists today offers a meaningful margin of safety.

Diamonds In the Rough: Viator and TheFork

The two other businesses within TripAdvisor, Viator and TheFork, have received little attention from the market until now. This may be because they are currently being managed for growth rather than profitability. It could also be because management provides little detail on them. Regardless, they are both very high-quality and fast-growing companies that could be worth more than the TripAdvisor Core business itself.

Like the hotel space, various economic characteristics make the tours and attractions OTA and online restaurant reservations markets very attractive for dominant players. First, they are both characterized by strong network effects. For example, in the case of Viator, consumers are more likely to use the platform with the most available attractions and reviews. More customers, in turn, draw more attractions to list on Viator, thus reinforcing the network effect.

In addition, both markets face significantly fragmented supplier bases, which are in a fixed-cost position. Hence, suppliers are willing to pay a high commission to acquire more customers, which drives operating leverage in their businesses.

Leading businesses in both markets should, therefore, exhibit similar margins to the leaders in the hotel OTA industry. Management has confirmed this in 2Q22: "although currently not yet demonstrating their profit potential as we invest in growth, we believe longer-term both Viator and TheFork can reach EBITDA margins of 25% to 30% given their strong gross margin profiles potential for scale, given their large TAMs and attractive unit economics."

Management may well be downplaying the margin profile should the businesses become dominant in their markets. For example, when TheFork's North American counterpart, OpenTable, was acquired in 2014, it had EBITDA margins of 41.2% in its mature North American business.

For its part, Viator is well placed to become the dominant tours and attractions OTA in its markets. It is currently by far the leading player, with a market share of 55% globally in terms of listings as of 2018, followed by Get Your Guide (20%), Expedia (12%), and Airbnb (16%).

It is targeting a large and growing market. According to Arival, in 2019 the tours, activities, and attractions market comprised $254 billion in gross bookings. In addition, the market is very much underpenetrated. Only 17% of bookings are done online, and less than 5% through an OTA. By contrast, OTAs account for roughly 25% of hotel bookings. As a result, the tours and attractions OTA industry is set to grow by >20% in the coming years.

While TheFork has a presence in the Europe, Latin America, and Australia, today it is primarily focused on Europe, where it has a dominant market position in many of the markets it serves. In 2019, Bertrand Jelensperger, senior vice president of TripAdvisor Restaurants, and founder of TheFork, stated that the company had "upwards of 40 percent […] market share in European countries, such as Spain, Italy, and France."

These markets in which TheFork has a leadership position are also very large. In 2018, full-service restaurants and cafés in Spain, Italy, and France generated sales of $45 billion, $57 billion, and $38bn, respectively, according to PwC. Capturing just a share of those revenues could drive substantial growth for TheFork for several years. Previous to 2021, Viator and TheFork were combined into one segment called Experiences & Dining. This segment grew at a CAGR of 31% from 2017 to 2019.

Management Team: New Management backed by Experienced Board

After more than 20 years at the helm of TripAdvisor, co-founder and CEO Steve Kaufer stepped down in 2Q22. He was replaced by Matt Goldberg, a veteran media executive who has held senior roles at Lonely Planet, QVC, News Corp, and The Trade Desk. Long-time CFO, Ernst Teunissen, also stepped down in October 2022 and was replaced by Mike Noonan, the former Senior Vice President Finance and Head of Investor Relations at Booking Holdings. It is not yet entirely clear what the strategy and execution will be like going forward with the new management team. While this introduces some additional risks, I think the change should be a net positive in that it could improve on TRIP's history of execution and bring fresh perspectives.

The management is backed by a highly experienced and capable board. Greg Maffei is the Chairman of TRIP and Chairman, President and CEO of TripCo. He is well-known among investors for the success he has achieved within the Liberty universe in partnership with John Malone. Greg O'Hara is the Vice Chairman of TripCo and a TRIP board member. He is the Founder and Senior Managing Director of Certares, a leading private equity firm focused on the travel industry. The firm's notable investments include American Express GBT, Hertz, and LATAM. Maffei and O'Hara are both aligned with shareholders given their significant economic interests in the company (although voting power and economic interests are somewhat nuanced due to a complicated holding structure).

Valuation: LTRPA – A Long-dated Call Option on TRIP

In the following table, I first detail my valuations for the respective businesses within TRIP according to my bear, base, and bull case scenarios. I then use the resulting TRIP value to arrive at my valuation for TripCo's NAV by subtracting the value of its net debt and preferred equity from its 21% TRIP stake. Finally, I compare the resulting NAV to the market cap of TripCo, adjusted for the implied market cap based on the price of its A shares (LTRPA).

Below, are my valuation assumptions for the different businesses in my bear, base, and bull case scenarios. First, however, I would like to make a few general comments.

I tend to agree with the view that TRIP's core metasearch business is a melting ice cube in the long term. It faces tough competition from Google, which sits directly above it on the customer acquisition funnel and can draw from its other products to improve the customer experience. If this is the case, the question then becomes, how long does it take for the ice cube to melt? The TripAdvisor brand and user reviews attract a lot of organic search traffic to the platform, which should be fairly sticky over time given that customers prefer to compare across several websites before booking (38 sites on average according to Skift).

In the meantime, the metasearch business generates a ton of cash. In 2018 and 2019, it generated $344 million and $341 million in Free Cash Flow, respectively. In addition, the company cut $200 million in costs in 2020, about $100 million of which are expected to stick. Therefore, as the business continues to recover from the pandemic, it could produce about $450 million in Free Cash Flow, or c.$350 million after accounting for stock-based compensation costs (11% FCF yield). Given this, even under very pessimistic assumptions, the metasearch business should be worth at least $1.2 billion.

Of course a global recession has the potential to depress travel, and TRIP’s earnings, in the short-term (although this may be offset by pent up demand following the pandemic). However, I believe that my bear case c.4x P/FCF valuation more than accounts for any recession-related disruption to earnings. In addition, TRIP has the balance sheet to weather a recession and continue to invest in the growth of Viator and TheFork, a benefit which its smaller competitors do not have.

Aside from my own estimates, we can draw upon a few private transactions as a sanity check for the Viator and TheFork valuations. In April 2019, GetYourGuide, Viator's closest competitor raised $484 million in a funding round led by SoftBank's Vision Fund at an over $1 billion valuation, with rumors of the valuation being as high $1.78 billion, against the company's 50,000 attractions listings and $192 million in sales (P/S of 5.2x-9.3x), according to PitchBook.

Based on the revenue multiple of this transaction, Viator could be worth between $1.7 billion and $3.0 billion on its LTM revenues of $324 million. Interestingly, in 4Q21, management indicated that "[it] recently submitted a confidential S1, which, along with other opportunities [they] are evaluating in parallel, puts [them] in a position for a potential sub-IPO of Viator, subject, of course, to market conditions." This could unlock some of the hidden value that exists in Viator.

In 2014, Priceline (now Booking Holdings) acquired OpenTable for an Enterprise Value of $2.6 billion. In 2016, it then wrote down the value of OpenTable to $1.6 billion due to a disappointing international expansion initiative outside of the US. This written-down value (which was close to what the public markets had valued OpenTable at before the acquisition) represented 8.3x its revenues of $198 million and 31.0x its EBITDA of $53 million. Using the OpenTable acquisition's EV/sales ratio, TheFork could be worth $979 million on its LTM revenues of $118 million.

When it comes to TripCo, given its capital structure, I see the shares as being akin to 1/5th of a long-dated call option on TRIP shares, with a strike price equal to the price of TRIP at which the NAV of TripCo would equal zero. I estimate that price to be $14.38. Interestingly, TRIP's January 2024 call option with a $15 strike price is trading at $10.95, compared to the current price of LTRPA shares of $1.20. If one wanted to reduce downside risk, one could short TRIP call options and go long LTRPA (the ratio would depend on how much one would want to reduce downside/upside).

Finally, a few housekeeping notes on some complicated aspects of the capital structure at LTRPA:

Greg O'Hara's firm, Certares, owns $187,414 worth of an 8% Series A Preferred Stock issued by TripCo. The value of this Preferred Stock increases according to an accretion factor with respect to the TRIP common stock equal to 0.8 times the percentage increase in the shares above a price of $17.08

TripCo also issued $227 million in Exchangeable Senior Debentures due 2051 which convert into 4.7 million shares of TRIP at a conversion price of $69.78

TripCo has two share classes: 72.5 million shares of Class A and 3.4 million shares of Class B common stock. The two are identical in their economic interests, but the Class A stock (LTRPA) has one vote per share, while the class B stock (LTRPB) has ten votes per share. Also, the class B stock is exchangeable on a one-for-one basis for class A stock, but not vice-versa.

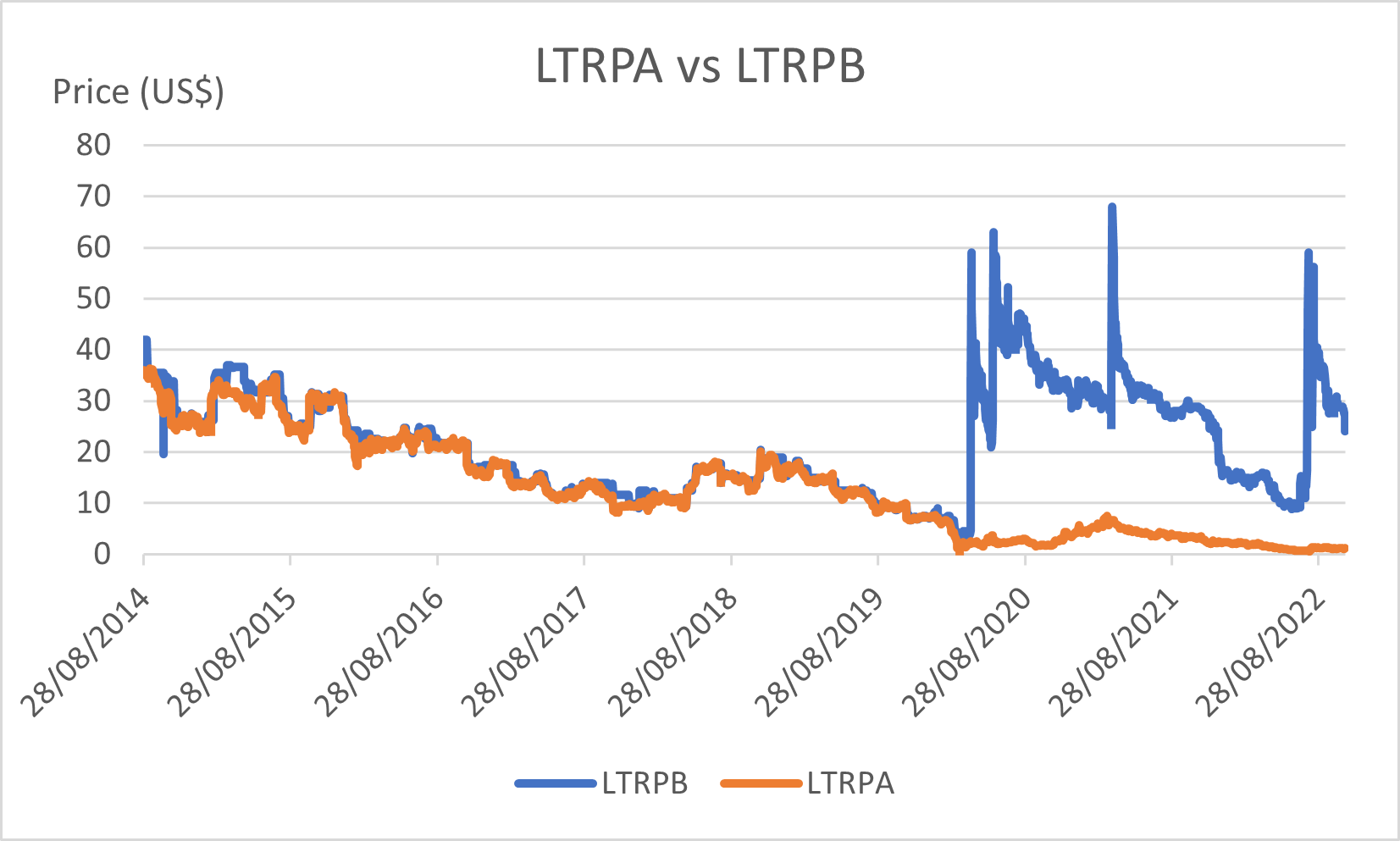

Class B stock currently trades at $27.20 vs $1.20 for class A stock. I see no fundamental reason why B stock should be worth significantly more than class A stock, so I have adjusted the market cap to assume that class B stock trades at $1.2. Just to prove how much of an anomally this is, I have provided a historical comparison between the prices LTRPA and LTRPB in the appendix

Valuation Assumptions

Appendix

Source: Company filings

Note: Average Monthly Unique Visitors from 4Q19-1Q22 are estimates. Average Monthly Unique Visitors in 1Q20 not available.

Source: Bernstein

Source: Yahoo Finance

Nice writeup. What's your current thoughts on LTRPA?

Well done you discovered treasure! Next write up should be $LiLAK. Sub 5 EV/Ebitda, buying back 10% of shares a year, FCF increasing over the next few years from synergies and a JV. Spin off, John Malone bought, CEO bought, buy back in place and leverage.